QCDs or Qualified Charitable Distributions transfer money from pre-tax accounts directly into a Charitable account. This direct distribution of pre-tax dollars to a charity will not be recognized as income and not added to your tax filing since it is under a QCD transaction. The distribution sent to the charity is usually part or the entire annual RMD (required minimum distribution) amount. QCDs are often used when they help avoid income taxes and increased Medicare premiums for RMDs that are not needed to fund lifestyle spending.

The pairing of QCDs and RMDs used occurs at the same age but not anymore. This has created a disconnect between the QCD and the RMD age for regular pre-tax accounts. QCD rules permit that QCDs begin at age 70½ but Required Minimum Distribution (RMD) age has changed from 70½ to 73+ (depending on your birth year) on saved regular pre-tax accounts. Since there is no requirement to make a pre-tax distribution until age 73+, QCDs shouldn’t be used until the start of RMD age.

On the other hand, for inherited IRAs, QCDs can begin at age 70½.

If you are considering retiring early and would like to use your pre-tax retirement accounts before age 59½ then you have significant planning to ensure you make the most of your retirement assets. One possibility is to use a 72(t) exception to avoid the early withdrawal penalty from pre-tax accounts. This 10% penalty is in addition to ordinary income tax.

An exception to the 10% penalty is the 72(t)(2)(A)(iv) OR “a series of substantially equal periodic payments (not less frequently than annually) made for the life (or life expectancy) of the employee or the joint lives (or joint life expectancies) of such employee and his designated beneficiary”. This exception allows for regular payments from pre-tax accounts but must be tailored to your specific situation.

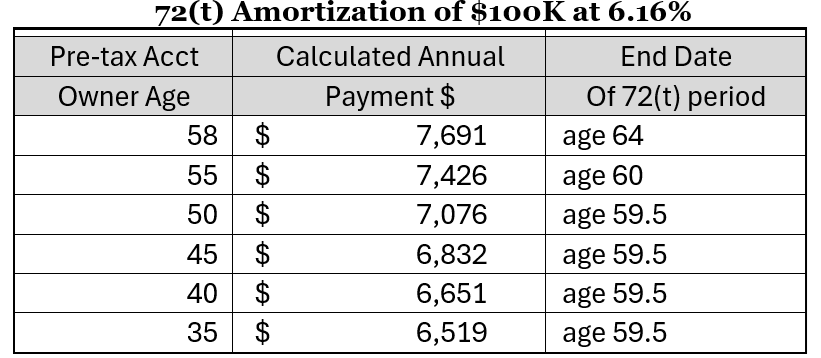

In general, the 72(t) exception requires that a calculated payment be withdrawn from a pre-tax account annually for the longer of five years or at age 59½. The advantage is that the 10% penalty can be avoided but the disadvantage is that changes to withdrawals or distributions are NOT permitted, or penalties apply. When calculating the annual payment, we consider the age of the pre-tax account owner, the balance in the pre-tax account, and the current interest rate. Higher payments are obtained at later ages, with higher account balances and at higher interest rates.

To help you visualize how the 72(t) amortization works, the table below shows annual payments for a single person at different ages on an account with $100K in pre-tax savings given that the current interest rate is at 6.16%.

Those thinking to retire early should consider using pre-tax assets (with the 72(t) exception) to support their planned cash flow but only if it is the best way to deploy all available assets. When using the 72(t)-exception you need to understand the implications of the rules since large penalties apply for errors or misunderstandings. If you are considering retiring early, we would determine how to best deploy your assets throughout your retirement plan.

Effective April 1, 2024, accounts held under the name of a trust will be insured by FDIC for up to $1.25 million, rather than the current $250,000 limit. Revocable trust (which include informal trust accounts such as Pay on Death (POD) or As Trustee For (ATF)) accounts are insured up to $250,000 per beneficiary per FDIC bank.

If we have created several taxable accounts at different FDIC banks, we may be able to consolidate into fewer accounts with higher balances (while retaining FDIC protection) if the trust has more than one beneficiary (to a maximum of 5) after April. We will review this at our meeting(s) if it is relevant to your finances.

The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on retirement planning. Specifically, the law stipulated that “Non-Eligible Designated Beneficiaries” (i.e., neither surviving spouses or disabled/minor beneficiary) would be required to empty the inherited retirement account by the end of the 10th year after the decedent’s death (and would no longer be able to ‘stretch’ the distributions over their own life expectancy).

While we expected that Non-Eligible Designated Beneficiaries would not be required to take annual distributions in addition to emptying their accounts in the 10-year period, the IRS in February 2022 issued Proposed Regulations that would make a subset of these beneficiaries subject to BOTH the 10-Year Rule and annual Required Minimum Distributions (RMDs). The caveat, however, was that these were merely proposed regulations.

In October 2022 we were informed that there wouldn’t be a penalty if beneficiaries didn’t take a 2022 RMD but by October most had already! Unfortunately, they failed to address the requirements for 2023 and onward.

Finally, this month the IRS released Notice 2023-54, which provides relief once again by eliminating any penalties for failing to take (potential) RMDs for 2023 for these specific beneficiaries. Once again, they punted the RMD decision another year (2024). Keep in mind that these beneficiaries MUST still empty the IRA account by the 10th year.

Although we monitor notices on RMD rules changes and discuss RMD requirements with each of you as needed each year, your engagement in this topic ensures that we understand the relevant regulations for your financial plan.

The State of California has clarified that the extensions will apply not just to IRS filing but also state filing for those counties detailed in the last newsletter. The extension lasts until Oct 16th. It includes tax-advantaged contributions and estimated tax payment for the fourth quarter of 2022, and those in 2023. If you haven’t already made your 2022 contributions, please verify with your tax preparer. Keep in mind that the extension is only available to residents from areas designated as disaster zones by FEMA (Federal Emergency Management Agency). In California it appears to be all counties except Lassen, Modoc, and Shasta. If needed, the extension can be useful and provides those impacted more flexibility, but we still recommend that you make every effort to complete your 2022 tax preparation as soon as possible.

The first “Setting Every Community Up for Retirement Enhancement” Act (SECURE Act) was passed December 2019 eliminating the ‘stretch IRA’ for non-spouse and changing the RMD (Required Minimum Distribution) age to 72. These were changes that impacted everyone across the board. With the Secure Act 2.0, congress appears to be reversing its prior leanings and instead allowing Roth conversions. The reversal towards ‘Rothification’ (encouraging ROTH savings/conversions) appears to be with the goal of increasing tax revenues today. It is fair to say that no single provision made by the SECURE Act 2.0 appears to have the same impact across so many as the elimination of the stretch, which now requires many inherited distributions to complete within 10 years, rather than spreading distributions over the entire beneficiary’s lifetime. Even so, 2.0 has so many more detailed provisions that it will impact most in some way. It is already evident that implementation will take more effort than the first SECURE Act.

Some of the new provisions included in SECURE Act 2.0 will be implemented over the next two years and require preparation in 2023. We will explore the provisions that may be relevant to your specific situation during our meetings this year. Let us know if you have any questions.

The details of the American Rescue Plan 2021 are still being processed BUT we know that it doesn’t include RMD relief for 2021 nor increased minimum wage. It does provide both 2020 and 2021 tax filing items. Below, I’ve outlined those that I found most significant so far.

“Stimulus Checks” For individuals: $1,400 per eligible individual for all dependents with stricter phaseout that start at $75K for individuals and at $150K for those married filing jointly (MFJ). File early if your 2019 tax filing does not qualify you for this stimulus.

Expansion of Child Tax Credit: It provides an increased amount of child tax credit for those under $150K (MFJ) AND an increase to $400K (MFJ) in earnings for the base credits. In 2021 there should be an opportunity to receive more child tax credits for up to $400K.

Extension of Unemployment Compensation: An additional weekly $300 Unemployment benefit was added, and coverage was extended until September 6th, 2021.

2020 Tax-free Unemployment Insurance income: For those receiving Unemployment Insurance in 2020, up to $10,200 of those earnings will be tax-free.

Increased Premium Credit Assistance: Healthcare premium assistance extended from 2020 through 2021 with higher earnings.

Tax Credit for Employers to cover COBRA for 3 months: Any employee involuntarily laid off will have free full COBRA coverage for 3 months by the employer who will receive credits for paying their COBRA.

Tax-free student loan forgiveness for the future – if a student loan is forgiven by 2025, it will be tax-free.

It will take time to distill what will be relevant for 2021 taxes particularly since we are all still trying to understand and work through CARES 2020 tax rules and implications for 2020. For now, it makes sense to slow down the 2020 tax filing and ensure that your CPA is aware of all of the CARES 2020 and TARP 2021 rules before filing – luckily, we all now have until May 17th.

Tax-deferred savings (to an IRA or employer pre-tax retirement plan) reduce your tax liability today BUT are fully taxable (including gains) on withdrawal. The tax-deferral accounts are an excellent way to minimize your current taxable income. The goal is to use what would have been tax dollars as part of your savings. The main rules to keep in mind are that withdrawals shouldn’t be expected before age 59.5 AND that you MUST take mandated distributions (called RMD) when you reach age 72 (according to the new tax rules). Unfortunately, these accounts are now also not inherited in the same beneficial manner as in the past (these now follow the new Secure Act of 2019 rules).

A Roth on the other hand, doesn’t provide tax deferral when saved but it does provide tax-free dollars, on withdrawal. Contributions to a Roth are limited in amounts each year and not easily available for high earners. Whereas Roth conversions require income tax payment on converting pre-tax IRA dollars, not everyone is permitted to make Roth conversions. Fortunately, Roth IRAs are not impacted by the Secure Act of 2019 and remain free of RMD. They are also still inherited tax-free to individual or trust beneficiaries and are likely to be favored for those considering leaving a legacy.

As income tax rises (likely, given our debt load), Roth accounts will become even more powerful tools in retirement for those in the higher tax brackets. Currently they help us regulate your taxable income and keep taxes and Medicare costs reasonable during retirement.

We’d like to consider Roth conversions for you in years when you expect a lower tax rate. It is particularly useful when tax-deferred accounts are undervalued and when you have accumulated large tax-deferred accounts.

The basic takeaway is that a tax-deferred account should be maximized during years with high earnings (to reduce taxes) and high tax rates. When you expect a low earning year then a Roth conversion may provide you with an ideal situation BUT ONLY IF your retirement tax rate is expected to be high enough to trigger additional taxes or Medicare costs.

As you know, we believe strongly that managing tax liability is essential to building wealth. The Secure Act of 2019 has made significant changes which we will use to create and action strategies best suited for each of you. Everyone, near retirement, is aware that there was an extension to the Required Minimum Distribution (i.e., RMD) from age 70.5 to age 72. This is good for many since it gives you more control over your tax liability early in retirement, but it also has made the Roth accounts an even more powerful tool for some.

Sadly, the Secure Act of 2019 has made inherited IRAs a big tax burden for beneficiaries, particularly trust beneficiaries. Because of this, IRA accounts that use a trust as a beneficiary may need to be re-examined to ensure that the language allows beneficiaries to minimize their tax liability. Let me know if these topics are of interest and we’ll include them at our next financial planning meeting.

I’ll quickly summarize

the impact of the TCJA (Tax Cuts and Jobs Act) that we’ve observed on personal

taxes and then I’ll switch to the impact on small business owners by covering

QBI (the Qualified Business Income) and changes to deductions.

The tax bracket has

dropped significantly for personal federal taxes since the top

rate is now 37% AND the higher tax brackets begin at much larger taxable

income. Though this sounded like a great opportunity to reduce the family tax

liability it was combined with drastic changes to the estimated tax deductions

and elimination of exemptions. The net result for residents of high-income

tax rate states (such as California) and who used Schedule A itemized

deductions is that their taxes actually increased. Most others found no change

or a small reduction in their tax liability in 2018 from the new rules EXCEPT

for small business owners. We expect the same in 2019.

Small business owners have a unique new tool in

the TCJA – the QBI deduction. This tool provides a real opportunity to reduce

taxable income and therefore tax liability.

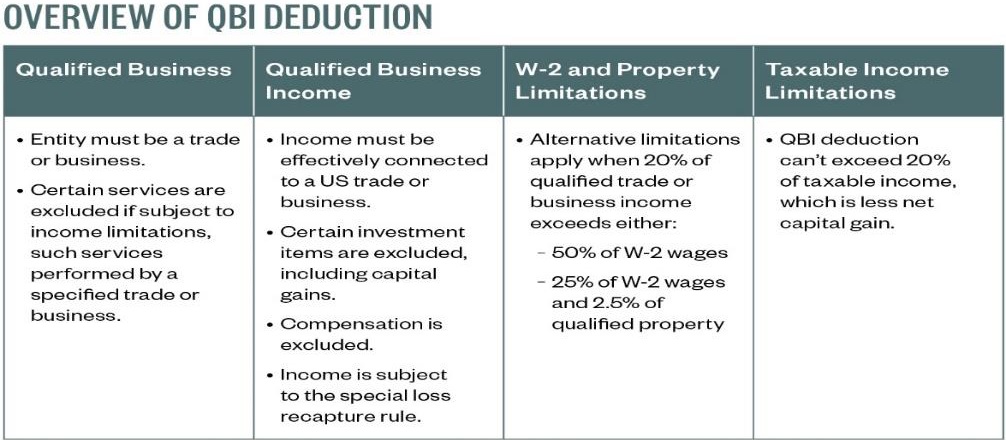

The QBI deduction is

available from 2018-2025 and is only for pass-through entities (businesses that

are not C Corporations). This deduction is available without income

restrictions for businesses that are deemed a ‘Qualified Business”.

The chart above specifies that to qualify for

this deduction you must be a Qualified Business. To be a Qualified Business it

can’t be a service business or be a trade or business that involves the

performance by the employer of services as an employee. The following are NOT a

Qualified Business: doctors, lawyers, accountants, performers, athletes, health

care professionals, financial and broker service providers, partnership

interests. Only two service providing businesses are considered a Qualified

Business: engineering and architectural firms. Though unclear in the code as to

how gray areas would be decided the key catchall is that you can’t be a

‘Qualified Business’ if the business’ principal asset is the reputation or

skill of one of the owners. Most of our clients own excluded (non-qualified)

businesses.

As an excluded business owner (such as

attorneys, consultants, etc.) you MAY STILL qualify for this QBI deduction IF

your personal taxable income falls below the limits of $315K and $157.5K

(married filing jointly and single filer respectively).

The QBI rule allows a Qualified Business (or

excluded businesses that qualify under the taxable income limits) to reduce

their taxable income by 20% of their QBI (QBI is business profit, not W2

income). An IMPORTANT CAVEAT is that the 20% deduction is the lesser

of QBI or taxable income.

For example, if your business profit is $200K

and your taxable income is $100K the actual deduction is $20K not the $40K that

you might have expected. Regardless this new tool does provide for a way to

reduce taxes.

When I initially reviewed the code, I was very

excited for the Qualified Businesses owned by our clients since they were to

benefit regardless of income. It was not until the last few months that a

complicated wrinkle has limited this excitement. We’ve found that even

Qualified Businesses have hurdles if the taxable income exceeds these same

limits ($315K/$157.5K for married filing jointly and single filer

respectively). If the business owner’s taxable income exceeds these income

limits, then two additional rules are used rather than just receiving a

deduction of 20% of QBI. For Qualified Businesses in excess of these limits

there is a two-pronged test to measure the lesser of 20% of QBI (profit)

OR the greater of either 50% of all W2 wages or W2 wages plus 2.5% of

your qualified equipment/land costs. Yes, after jumping all of these hoops we

found that some QB businesses didn’t qualify for 20% of QBI because the W2

weren’t high enough. Even so, the business owner did obtain a deduction though

not as high as was initially estimated.

Added to the QBI deduction the TCJA rules also

include these changes:

1. Entertaining clients is no longer a business

expense that is deductible federally (it used to be 50% deductible). Office

parties are still 100% deductible.

2. Businesses supported by debt financing can

only deduct 30% of the owner’s adjustable taxable income BUT don’t despair

since it will only apply to small businesses that have gross receipts of $25M

for each of the last three years.

3. NOL deduction (Net Operating Loss) which is

often carried back two tax years or future 20 years will now be only allowed

for years going forward AND limited to 80% of income in that year.

I’m providing this

education article to give perspective on how you benefit from the TCJA tax

rules. Our ultimate goal is to have you knowledgeable enough to understand the

critical role of taxes in your planning. If you have additional questions feel

free to ask us or your tax preparer.