Tragically, there are countless stories of victims losing their entire life savings to texting/phone/email schemes. Adding to this is the evidence that many of the scammers are from forced labor situations. The best way to avoid becoming a victim is to adjust OUR BEHAVIOR. Do NOT respond.

You should never respond to unsolicited texts or unsolicited conversations about loans or investments or money. If you do get caught in a scam, your best defense is to NOT feel embarrassed and get out as soon as you can, even with a loss.

Before making investments, reach out to AIKAPA or a knowledgeable trusted person for a second or third opinion. Ideally you will be able to ignore these types of contacts.

If it becomes clear that it is a scam, then file a complaint on the FBI’s Internet Crime Complaint Center (IC3): https://www.ic3.gov. If it is related to crypto assets, then also report it to cryptofraud@usss.dhs.gov and the Secret Service will refer your email to an appropriate field office for immediate action.

We define our lives by the decisions we make every day. Whether it is an unexpected or unwanted election result or life transitions like death, divorce, or job loss, how we deal with these crises will define who we are (and who we become). It is tempting to wallow in self-pity, obsessing about worst case scenarios, engaging in bitterness and blame, or spending to forget, but these will only hurt and control your life. These behaviors will not provide lasting satisfying experiences or happiness within yourself. I encourage you to take the time, this year-end, to examine how you handle uncertain or stressful times and what actions you can take that will create positive experiences that will make you stronger, more resilient, and empowered.

Think about the good, the bad, and the ugly and decide what you want to keep or change in your financial life. Below are some thoughts on financial strategies to consider.

• Build up an emergency reserve. We typically recommend that two-income families (with kids) maintain a reserve equal to six months of living expenses and nine months for one-income families. Couples without kids can keep their reserves at 4 months of living expenses and single earners need at least 6 months. During stressful times you may want to increase these amounts if you become concerned about the future. Let us know and we can help you define and create your reserve.

• Pay down debt. These days unnecessary debt is very expensive, so consider paying down any unnecessary debts, such as credit cards, car loans or home equity lines of credit (anything with an interest higher than 4% should be paid – anything below should be aligned with your financial goals)

• Review your cash flow (or budget) each month to keep you financially connected.

• For those who spend during stressful times … I encourage you to engage in “Stress saving” as opposed to “Doom spending”. The savings will add to your safety net and make you feel more stable and secure whereas an increasing credit card balance adds stress and uncertainty. By focusing on strengthening your savings you’ll become more resilient in the face of uncertainty.

• Focus on gratitude and the things that make you smile. If you’re feeling unhappy with the world right now, focus on what you’re grateful for. The evidence is clear that being grateful and smiling each day can help improve sleep, lower stress and enhance relationships. Practicing gratitude can be a powerful antidote to the negativity we may feel around us, especially when the things worrying us are beyond our control. Find time to acknowledge each day the good things in your life.

If you’re feeling anxious and stressed, anchor yourself to what you can control and give yourself permission to release what lies beyond your sphere of influence. Remember, as Seneca The Younger wisely observed, “We suffer more in imagination than in reality.”

If we’re honest with ourselves, most of what we fear never comes to pass. Or if it does, it often brings unforeseen opportunities for growth or positive avenues for change. So, during this upcoming holiday season, if you’re feeling fearful or have a sense of doom and uncertainty, focus instead on strengthening your financial foundation, practicing gratitude, and managing what you can control. In time, you’ll feel more confident and better equipped to face whatever the new year brings our way.

There is no crystal ball on what will happen with mortgage rates in the future. This quarter, I’ve been asked, several times, for my thoughts on future mortgage rates. According to Government-sponsored enterprises forecasts, the mortgage rates this year (30-year mortgages) will remain over 6% and possibly drop to at most 5.60% by end of 2025. The commercial bankers (MBA) forecast are a bit higher at 6.60% this year and 6.4% by end of next year. Most recently, both Fannie Mae and MBA stated that they expect mortgage rates to remain above 6% in 2026 though keep in mind that without knowing inflation rates, growth rates, and employment rates these predictions are not reliable.

The question that usually follows has different answers for different people – Should I hold out for lower rates before a refinance or house purchase? If you want an answer for your situation then always have us run the numbers regardless of whether you are considering refinancing, buying a new home, or paying off your mortgage. In general, keep in mind that expected changes in mortgage rates this coming year are NOT significant and should not play a big role in your home purchase decision. On the other hand, it is significant to consider the cost of your mortgage over the next five years and the impact the mortgage will have on your cash flow.

Of course, the most common question is whether mortgage rates will ever go down to 3% again. Mortgage rates have seldom been at 3% or lower. This low rate only occurs in extreme times, (such as during the peak of the COVID-19 pandemic). We don’t know if rates will drop significantly in the next years BUT we do know that economic conditions need to deteriorate significantly for rates to fall that low again.

Perceptions, including beliefs and media noise about which political party will be better for investors, can create anxiety and regrettable investment changes.

Consumer Confidence by Political Affiliation

The purpose of your portfolio strategy is to provide growth from expected business profits while minimizing the downside, regardless of election outcome or latest media trend. Once we know the election outcome and the likely policy platform of the new House, Senate, and President, we may adjust the portfolio strategy.

In theshort term, we will monitor for market opportunities stemming from market-based investor greed or fear.

For families with college students know that financial aid form filing time has arrived. Unlike last year’s rocky rollout of the new FAFSA application, this year’s form appears to be relatively glitch-free. If you’re debating whether to complete the FAFSA, here are a few reasons why it’s worth the effort even if you don’t think you’ll qualify:

1. You might qualify for need-based aid. Many families assume they won’t qualify, but they might. This is especially true considering that a surprising number of schools have a cost of attendance that can approach $100,000 per year.

2. To prepare for possible changes in your financial situation. If your financial situation changes in future years, most schools (~90%) won’t allow you to apply for need-based aid if you didn’t file FAFSA before your child’s first year of college.

3. Access merit-based aid. Some schools (~25%) require students to complete financial aid forms, including the FAFSA, to be considered for merit-based scholarships. It’s worth asking each school your student is applying to whether this applies to them.

4. Secure federal student loans. Even if you don’t qualify for need-based aid, filling out the FAFSA is necessary to access federal unsubsidized student loans. These loans don’t require credit checks, often offer favorable interest rates, and provide flexible repayment options. Additionally, your child will start building their credit history while in college, even though payments aren’t required until after graduation.

Fortunately, the FAFSA process has been streamlined and is now much easier to complete. For example, many families will have their income data transfer automatically from the IRS. Below are my suggestions to keep the process smoother:

Do NOT include retirement accounts under parent or student investments.

Do NOT include primary home equity under parent investments.

Do NOT include parent-owned 529 accounts for other siblings under parent investments, nor any grandparent-owned 529s.

Do NOT miss the chance to select “Yes” for a work-study job on campus.

Do NOT assume your Student Aid Index (SAI), previously known as the Expected Family Contribution (EFC), is the actual amount you’ll pay at each college.

Do NOT overvalue your business or secondary real estate.

Do NOT miss deadlines. Some school aid is first-come, first-served.

It is always a smart move to complete the FAFSA application for ALL college-bound students though in the past the process was too intrusive and laborious. It’s now a much simpler process, and with these suggestions, it shouldn’t take long.

With college costs rising, it’s worth exploring every opportunity to reduce expenses. Let us know if you would like to discuss the financial plan you have for your college-bound loved ones.

The purpose of the Corporate Transparency Act (CTA) is to create a national database of those who control entities in the US (including owners, principals, control persons of LLCs, C Corp, S Corp, LPs, and other closely held entities). The database will identify the human beings behind these entities. This law is part of an increasing effort to combat money-laundering, terrorism, tax evasion, and other financial crimes. The stated goal is to provide law enforcement with the ability to strip “US shell companies” of anonymity that can hide illicit financial activity and funding of terrorism. But this database will require information from every entity owner and yet few business owners know about this upcoming filing requirement.

There are over 33 million small businesses in the US and an increasing number of bad players caused Congress in 2021 to enact the CTA [Ref 1] as part of the National Defense Authorization Act [Ref 2]. The CTA created a new reporting requirement for “Beneficial Owners Information” (“BOI”) to the Treasury Department’s Financial Crimes Enforcement Network (or FinCEN).

With the deadline for pre-existing companies to file approaching (January 1, 2025 and even sooner for new companies created during 2024) and court challenges not yet staying this deadline, small business owners (and other entity owners) need a deeper understanding of how to handle their own BOI reporting requirements.

Ultimately, most of our business/entity owner clients will file a relatively simple BOI report. Some companies/entities with more complex ownership and leadership structures might require the help of outside legal counsel since CPA/CFP are not legally permitted to interpret this law for clients. It is advisable to take the time to read over the FinCEN FAQs [Ref 3] and Small business Guide [Ref 4] and determine if your firm has to file and if so whether you will need legal advice to complete this filing. We can help guide you but can’t interpret the law for you.

Who Needs To Report Their Beneficial Ownership Information (BOI)

At a high level, any company that was created by filing a document with a secretary of state or similar state-level office in the U.S. is a “reporting company” or entity that is required to file this BOI report. In practice, the requirement applies to business entities like Limited Liability Companies (LLCs), Limited Liability Partnerships (LLPs), and corporations (C and S Corp) that are created by filing paperwork with the state(s) where they do business. It does not, however, appear to apply to unregistered entities like sole proprietorships and partnerships. In addition, there are 23 different types of companies that qualify for an exemption to the BOI. The FinCEN’s Small Entity Compliance Guide outlines the specific criteria that companies must meet to qualify for each type of exemption [Ref 4].

Please be aware that even if your company has been inactive or recently dissolved it may still need a BOI filed. Lastly, irrevocable trusts may also be required to file.

What Information will be Required?

The Beneficial Ownership Information (BOI) report itself is fairly simple and consists of 3 sections (plus an introduction page and a submission page): The first section requires business identification whereas the second and third sections request personal identification (this includes state ID, US passport or foreign passport). We encourage any beneficial owner to notfile personal information directly in the BOI but instead create a FinCEN Identifier number. Creating this unique FinCEN ID number by the beneficial owner will require the upload of personal financial identifiers only once (under this FinCEN ID). Once created the FinCEN ID can be used in lieu of entering personal information directly in the BOI filing.

Please keep in mind that this filing is a separate process from tax filings and requires disclosure of personal information. This privacy invasiveness has led to legal challenges earlier this year, but none have yet stayed the BOI filing deadline. Given that the penalty is up to $500 per day for failing to file we encourage you to determine how and when you will file your entities BOI. We will all continue to monitor the legal challenges and the filing deadline since there may be announcements just prior to year-end.

FinCEN has put together a comprehensive FAQ on the specifics of the requirements [Ref 3], as well as a Small Entity Compliance Guide that we recommend reading [Ref 4]. These should help owners understand their obligations under the new rules. Please familiarize yourself on what will or will not be needed for your firm/entity.

Reference Links mentioned above: [Ref 1] CTA details: https://www.fincen.gov/sites/default/files/shared/Corporate_Transparency_Act.pdf [Ref 2] National Defense Authorization Act details: https://www.congress.gov/116/bills/hr6395/BILLS-116hr6395enr.pdf [Ref 3] FAQ on BOI: https://www.fincen.gov/boi-faqs [Ref 4] FinCEN Small business entity guide on BOI filing: https://www.fincen.gov/sites/default/files/shared/BOI_Small_Compliance_Guide.v1.1-FINAL.pdf [Ref 5] BOI filing: https://boiefiling.fincen.gov/

The AIKAPA equity portfolio is a global portfolio intended to provide diversification of US capitalization with uncorrelated assets over the rest of the world as well as within the US. We evaluate and reset the Global allocation based on both risk and known capitalization for countries throughout the world annually and review it quarterly.

I thought you might find educational an overview of country specific public equity capitalization that we use each year to set the AIKAPA equity strategy. Capitalization is the available wealth from the business marketplace in each country – we measure the ability to generate income/wealth for the investor. World financial market capitalization size is not the same as the world’s landmass, population, gross domestic product, or even exports. We often divide World equity into Developed (at $72T or 88%) and Emerging ($10T or 12%) country public capitalization.

To gain perspective it is useful to understand that there are about 3,500 public companies in the US consisting of 61% of the World’s total market capital (this was about $50T at end of 2023) and yet ONE company (Apple) holds $3T of those assets which is about 4% of the World’s capital. This one large company holds more market capital than Canada or France and about the same as the entire UK!

December 2023 World Equity Partial List by Decreasing % Capital by Country * USA (3,481 companies) – 61% of World Capital ($50T) * Japan (2,557 companies) – 6% of World Capital ($4.7T) * UK (590 companies) – 4% of World Capital ($2.9T) * China (2,295 companies) – 3% of World Capital ($2.4T) * Canada (525 companies) – 3% of World Capital ($2.2T) * France (229 companies) – 3% of World Capital ($2.1T) * India (1,535 companies) – 2% of World Capital ($1.8T) * Switzerland (172 companies) – 2% of World Capital ($1.7T) * Germany (248 companies) – 2% of World Capital ($1.5T) * Australia (486 companies) – 2% of World Capital ($1.5T) * Taiwan (1,458 companies) – 2% of World Capital ($1.6T) (The data above is an excerpt from the 2023-Dimensional funds annual report and only includes a small number of countries for illustration purposes).

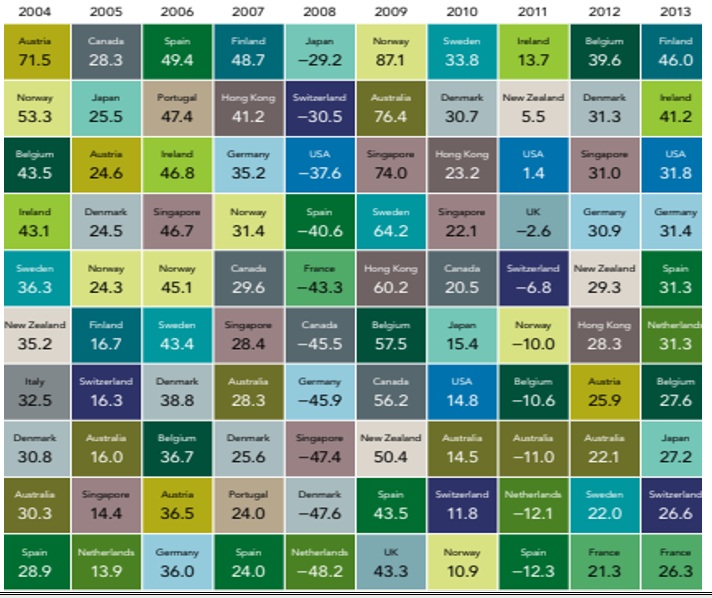

But Can We Select Which Countries Provide the Best Returns? Most people assume that the US is the best market performing country every year since it has the largest capital. The facts show that the US doesn’t always even make the top ten best performing developed countries. That said, the last 6 years have been unusual, from 2018-2023 the US has performed in the top 10 countries, in five out of six years (83%)! A major accomplishment. BUT it is a different story in the prior ten years. If we look earlier, from 2004-2013 (see chart below), we find that for 6 of those years the US was altogether missing from the top 10 performing countries. It only made the top 10 best performing countries 40% of the time.

If you look over the chart of the best performing developed countries below, you’ll also see that we can’t predict which country will do best in any year but by exposing the portfolio to other countries based on a combination of country capitalization and level of country risk we can improve the overall AIKAPA portfolio long-term performance. The largest impact is from increasing the probability of including exposure to countries that experience better performance when the USA under performs (uncorrelated countries). Looking for uncorrelated assets is an important way that a diversified portfolio generates higher long-term performance over other strategies.

Developed Market Countries Ordered by Equity Returns Each Year (2004-2013)

Modeling positive financial behaviors for the younger generation especially in affluent communities can pose unique challenges. Here are some key topics I’d like you to consider:

1. Understanding the concept of “enough”: In affluent communities, where material possessions are abundant, it’s essential to teach the young (and not so young!) that wealth is not solely defined by possessions. I like to keep my focus on President Roosevelt’s quote “Comparison is the thief of joy” and encourage a focus on spending that has lasting satisfaction rather than buying the next ‘in thing’. Usually, this includes understanding the role that money plays in their lives and how they wish to integrate financial security, spending, saving, and investing.

2. Value of Budgeting and Understanding their Spending: Teaching younger generations to follow and understand their income and expenses is crucial for financial independence and achieving life goals like homeownership and retirement. Helping them understand their spending patterns provides opportunities for money conversations and creates comfort around money conversations. The goal is to encourage them (however slowly) to plan their spending and create sustainable financial habits that will last them a lifetime.

3. Understanding the value of employment: Encouraging loved ones to recognize the value of a job or career is part of growing up. We all know that employment provides value beyond earning money since it can add unique opportunities. It will also provide them with a steady source of income, so they have money to eat out, do fun things with friends, and hopefully also begin saving.

Financial literacy for the younger generation is challenging since so much of their world is imbued by marketing. The challenge is how to model or engage with them not to crave what others seem to have but rather to understand what brings them long term satisfaction.

QCDs or Qualified Charitable Distributions transfer money from pre-tax accounts directly into a Charitable account. This direct distribution of pre-tax dollars to a charity will not be recognized as income and not added to your tax filing since it is under a QCD transaction. The distribution sent to the charity is usually part or the entire annual RMD (required minimum distribution) amount. QCDs are often used when they help avoid income taxes and increased Medicare premiums for RMDs that are not needed to fund lifestyle spending.

The pairing of QCDs and RMDs used occurs at the same age but not anymore. This has created a disconnect between the QCD and the RMD age for regular pre-tax accounts. QCD rules permit that QCDs begin at age 70½ but Required Minimum Distribution (RMD) age has changed from 70½ to 73+ (depending on your birth year) on saved regular pre-tax accounts. Since there is no requirement to make a pre-tax distribution until age 73+, QCDs shouldn’t be used until the start of RMD age.

On the other hand, for inherited IRAs, QCDs can begin at age 70½.

The Federal Open Market Committee’s last meeting (in May) clearly described their concern over stubborn inflation (at 3.4%) and indicated they would keep the same Federal interest rate (at 5.25%-5.5%) until inflation consistently approaches the 2.0% target. They were also in agreement to increase the interest rate if inflation and unemployment increases significantly. Next meeting is on June 11-12 (next week).

On the other hand, this month, we saw the first of the Group of Seven central banks kick off an easing cycle when The Bank of Canada cut interest rates by a quarter of a percentage point (now at 4.75%). The rationale provided is that inflation in Canada (measured at 2.6%) is heading towards the 2.0% bank target.

Is this a sign that the Feds will do the same at their next meeting?Maybe, if inflation has dropped below 3%.

Any drop-in interest rate is beneficial to those seeking a new loan or mortgage BUT the opposite is true for those seeking to retire early (before age 59½) and use an exception to withdraw from the pre-tax accounts without paying a penalty … see the ‘Early Retirement:’ article below.