The transfer from TDAI to the Schwab Alliance platform has been completed and I wanted to provide you with an update. We are still experiencing longer delays to complete tasks on the Schwab platform (than we did on the TDAI platform) but we have started to see improvements.

We have noticed that Schwab likes to email and send mailers far more often than we experienced when TDAI was the custodian. I would like to double down on my usual recommendation that you NOT click on hidden links within emails – Schwab appears to send many emails with hidden links. You could instead log into your Schwab online account directly and address Schwab’s emailed request. Our concern stems from potential spoofing of both the email and the Schwab website. Our priority should be to keep your Schwab Alliance login credentials safe and secure so that we can maintain digital safety of your portfolio. To do so please be sure you only log in using the Schwab legitimate website and from a safe electronic device.

Mid-January, Schwab sent an email to those who participate in the Schwab sponsored individual 401k plan regarding a new ROTH 401K plan feature. This is good news but for now, please ignore it. We can discuss how it works at our next meeting particularly if it might be useful for your financial plan.

If you are having difficulty logging into the Schwab Alliance website, please let us know. If you have not yet logged in to the Schwab platform then you will begin receiving paper reports in April unless you log into your account before March 27, 2024.

Social Security benefits were never intended to be the sole financial support during retirement but for 21% of retirees Social Security benefit is the only source of income. For most American workers, Social Security benefits are the only guaranteed retirement income that is also inflation adjusted each year.

All workers in America are entitled to pay into Social Security and based on their pay history, to receive a lifetime income each month starting from ages 62 to 70.

Ideally prior to retirement, you’ll also maximize other income sources that include taxable savings, IRAs, ROTH, Qualified plans (401K, 403b, 457b), annuities, deferred compensation, and employer pension plans.

Since your future Social Security benefit is calculated from your Social Security work history, you must ensure (and correct if necessary) that this history has been recorded correctly at www.socialsecurity.gov/myaccount OR the new www.ssa.gov/myaccount.

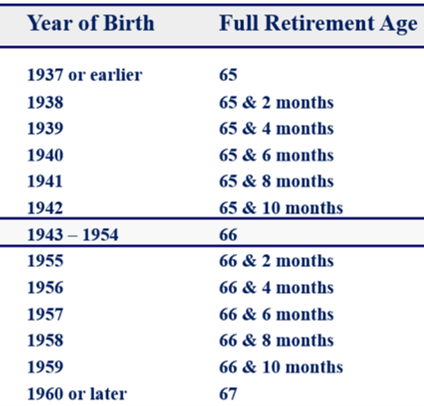

Social Security benefit calculation uses your top 35 highest earning years and projects your estimated benefit at your FULL RETIREMENT AGE (FRA).

Your FRA is based on your birth year and, as you can see on this table, it has been increasing. In fact, since 1983 when the FRA was 65, it has been increased gradually so that by 2025 (for those born in 1960 or later) the FRA will be 67. To understand Social Security, you must first determine your FRA.

When can you collect Social Security? At FRA, you can file and receive your full benefit (100%) based on the amount of Social Security tax paid to your Social Security number. The earliest you can collect Social Security benefits on your record is at age 62 (when your FRA amount is reduced ½% for each month or 6% less each year until FRA) and the latest at age 70. If you delay past your FRA, you earn Delayed Retirement Credits (DRC) and for each month it will grow two-third of a percent or 8% per year until age 70.

Example of how benefits are calculated: If you were born in 1960 and your FRA amount is $1K/month then collecting at age 62 will result in a lifetime amount of $700/month but delaying until age 70 would result in $1,240/month (plus annual COLA adjustment).

When creating your financial plan, we will consider different Social Security timing strategies based on your financial and longevity expectations. When deciding on your best timing we always request that you consider your health, your family’s longevity, and known increases in population longevity.

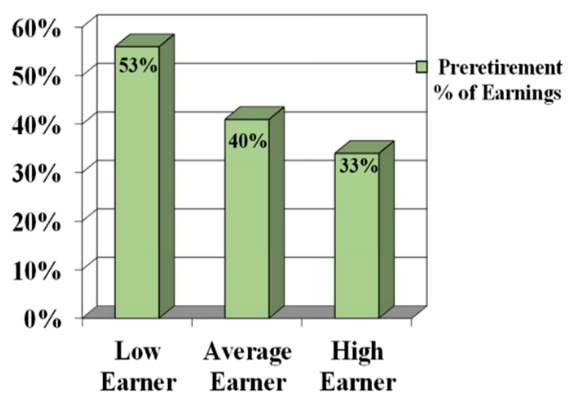

Compared to what you earned, what can you expect to receive? As an example, an average earner ($58K) could receive $1,907 or $23K per year in benefits for life, starting at FRA. On the other hand, those who paid Social Security at maximum earnings for 35 years would receive $3,822/month or $45K per year if 2022 was their FRA.

What if you take early benefits while still working? It seldom makes sense to work and take Social Security benefits early because your benefits are reduced by $1 for each $2 earned above an annually set earning level (in 2024 you can only earn up to $22,320 per year ($1,860/month) before your benefits are reduced). Once you reach FRA your Social Security benefits are NOT reduced (regardless of earnings).

We encourage each of you to work with us to review your Social Security history and then use your financial plan to make the best Social Security timing decision for you.

Applying for Social Security should be started three to four months prior to your chosen Social Security benefit start date. You would apply online at www.socialsecurity.gov or call (800-772-1213) or go to the local Social Security office. One last and very important cyber security reminder: Protect your Social Security log in information (or credentials) – make certain that you are using a secure device when you log into your account.

Effective April 1, 2024, accounts held under the name of a trust will be insured by FDIC for up to $1.25 million, rather than the current $250,000 limit. Revocable trust (which include informal trust accounts such as Pay on Death (POD) or As Trustee For (ATF)) accounts are insured up to $250,000 per beneficiary per FDIC bank.

If we have created several taxable accounts at different FDIC banks, we may be able to consolidate into fewer accounts with higher balances (while retaining FDIC protection) if the trust has more than one beneficiary (to a maximum of 5) after April. We will review this at our meeting(s) if it is relevant to your finances.

Though Bitcoin gets the Crypto headlines, I continue to remind you that it is Blockchain that is the promising digital technology that has a place in investment allocation in a long-term retirement portfolio.

Though in 2017 Crypto looked promising, in 2022 we saw the complete collapse of Terra (4th largest cryptocurrency and its related Luna coin) that was believed to be the most stable crypto (it was linked to US dollar) and in 2023 we saw the high-profile collapse of cryptocurrency exchange FTX (Sam Bankman-Fried was convicted of fraud and is awaiting sentencing in 2024). Bitcoin was at $64.4K in November of 2021 and the same single coin was worth $16,500 by November 2022 and was back at $34K by November of 2023. That is certainly too much volatility for a retirement portfolio and yet speculators, media, and pundits promote that it be included. The most stable Cryptocurrency platform and coin are currently Ethereum and its Ether coin, but it is still very volatile.

The progress and growth of Blockchain as a financial digital technology (rather than as a currency) has increased and it looks like it may be an important part of productive AI (Artificial Intelligence) technology development. In addition, Blockchain technology has already seen much revenue growth. Consider that the revenue was around $35M in 2019 and in 2023 increased to $1.75B.

As time passes, we are seeing more acceptance and conversation on how to best allocate digital assets in a portfolio. The most recent was the SEC acceptance of Cryptocurrency-based exchange-traded funds (ETFs) which are primarily for currency allocations. Unfortunately, we are also seeing danger signs. Use of cyber/virtual currency to fund terrorism and destabilize governments may be its undoing since a significantly large and obvious connection between Blockchain and terrorism will cause a global crackdown. My hope is that a crisis will instead generate protective processes/tools which may allow Cryptocurrencies to compete directly with fiat currency.

For now, Cryptocurrency is an investment to be consider like you might consider investing in art, collectible cars, rare coins, and stamps. It can gain and lose a lot of value and not be liquid to use in a crisis particularly during your retirement.

The FTC has made access to credit reports from the three major credit reporting agencies via www.annualcreditreport.com available on a weekly basis for free. This was announced at the end of October without much fanfare. Prior to COVID these reports were only available annually (for free) and during COVID the FTC made it temporarily available on a weekly basis. This is good news for consumers!

Start the New Year off with a review of your three credit reports. You will likely need your old credit report to sign-in – the identity confirmation questions are more difficult than in the past and may require that you reference your prior credit report. Once you download your new credit reports focus on ensuring that they correctly state your information and make corrections promptly if needed. We will go over credit history in a later check-in this year.

In 2024 we are expecting recoveries in some real estate categories, a settling of interest rates, and dramatic growth in the AI (Artificial Intelligence) space. It is the latter that could help businesses improve efficiencies and deal with headwinds from labor costs/shortages though it is still at its infancy. In addition, we are seeing growth in capital invested to deal with the expected scarcity in rare earth metals. If we have limited supplies then price volatility will greatly impact data, electronics, alternative energy, and agriculture investment sectors (new sources for these metals are from mining of asteroids and other stellar bodies).

The less predictable potential for volatility, in the USA, will come from our ability to deal with the destabilizing forces all around us from climate change and the election. I suspect that the US consumer will continue to spend through volatility and reward companies that meet the consumer demands (as they did in 2023).

I hope these “thought starters” will help close 2023 and make the most of 2024:

Acknowledge What Went Wrong and Move Towards your future: What’s done is done and we can’t go back and change it, so recognize the errors and the changes that need to be made. This is our challenge and our opportunity for 2024.

Be kind to yourself: Celebrate your Progress! Acknowledge how far you’ve come and “keep your eyes on the prize” despite any 2023 setbacks (job loss, death, overspending, disability, divorce, market declines, missed goals, procrastination etc.).

Measure What Matters: As Theodore Roosevelt said, “Comparison is the thief of joy.” Understand what matters to you and measure your progress towards achieving your goals.

Focus on What You Control: We can’t control other people, politics, the stock market, or social media but we can control what we think and what we do each day. Ever check an email or text only to look up 20 minutes later and find yourself scrolling on your phone, not knowing how you got there?! It is up to us to put in place ways to control our behavior and to hold ourselves accountable to our goals and values. This is particularly important when headlines fill you with fear. Don’t waste your valuable time on what you can’t influence or control.

Protect Your Wealth: Implement ways to protect your assets, life, health, income, personal information, family, and confidential data so that when a crisis occurs you can meet expenses and make the most of new challenges. We protect our wealth using insurance, updated legal documents, sufficient emergency savings, updated organized finances, and updated resources (lines of credit and portfolio). We work together to keep moving you towards your financial goals through life’s challenges.

Tax Allocation: Planning your taxes is essential to helping you to keep more of what you’ve earned. To make the most of opportunities we must work together to understand your base tax profile and adjust it through the year so that we can execute on available tax strategies by year-end. During high-earning years we often prioritize tax savings while keeping our eyes on the big picture that may indicate recognizing higher taxes to gain a future advantage.