What are the ingredients of a good portfolio?

If you do a little research, you will likely discover the three characteristics or criteria of a ‘good’ portfolio: (1) it should be diversified, (2) uses indexes, and (3) keeps costs low. All valid characteristics, to a point. In reality, this amounts to an over simplification that tells only part of the story. Applied to a poorly constructed portfolio, these characteristics will not help you create a good portfolio and you will not feel the confidence you need to see you through a market downturn. So, what is the best recipe for a ‘good’ portfolio—one that doesn’t cause you anxiety and keeps you up at night while generating long-term reasonable returns?

Here is my list of five ingredients for an effective long-term portfolio:

1. HAS A STRATEGY. First and foremost, your portfolio should follow a strategy that you believe will be effective. You need to understand and believe in it enough that you can allow it to capture value over time (while others are off chasing the latest trend). At AIKAPA we use a global investment strategy that leans towards value (rather than growth) allocations.

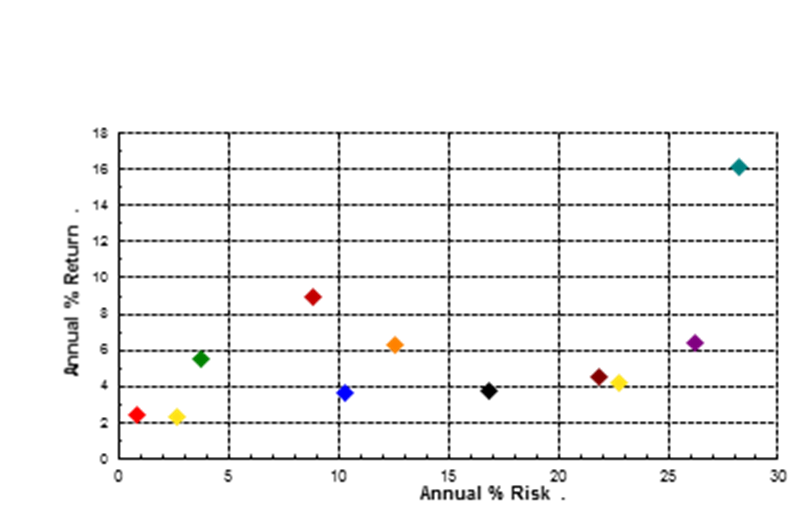

2. IS DIVERSIFIED. Select a diversification that represents your strategy and provides exposure to asset classes that behave significantly different from each other. In AIKAPA’s portfolio we are diversified across equities (that include large and small US and non-US equities) and across bonds, each global asset class providing opportunities to capture value. Using the chart below, you can compare global asset classes and how their volatility and returns differ from each other.

3. IS LOW-COST/HIGH-QUALITY (i.e., often an index fund). Implementing your diversified strategy needs to be completed using low cost, high quality securities. Use of baskets of securities (such as proven index funds) to represent chosen asset classes in your portfolio will permit the needed diversification while eliminating the risk associated with the failure of any one company (mutual funds or exchange traded funds are the baskets we use for your portfolio).

4. IS LOCATION SENSITIVE and TAX MINDFUL. Being mindful and “tax sensitive” when purchasing securities and locating them in the appropriate type of account can result in higher NET gains. Tax free, tax deferred, and taxable accounts should hold securities that will provide needed diversification, but will also yield the best AFTER tax returns. This approach is termed asset LOCATION selection. Taxable accounts are particularly valuable in the short and long-term but should hold assets that will not dramatically increase personal tax liability (particularly for those already in the higher tax brackets). As an example, two similar US Small capitalization funds can create very different tax liability simply by the level of “turnover” inside the fund. This turnover is often caused by frequent trading by the fund managers and can significantly reduce after tax net returns.

5. IS REGULARLY REBALANCED. Finally, we have rebalancing of a portfolio. Rebalancing by conventional wisdom is what enhances your long-term returns by periodically selling what is overpriced (over-valued) and buying those that are underpriced (under-valued). The reality is not quite that simple. Automatic rebalancing software, for example, is tempting owing to its simplicity, BUT can lead to high turnover and reduced gains. Keep in mind, rebalancing has at least two different purposes. Rebalancing across unlike return assets (for example between equities and bonds) will result in a decrease in long-term returns, while reducing volatility (or risk). Yes, you trade some upside to reduce the downside. On the other hand, rebalancing between similar return assets (such as, between equity funds of large and small capitalized companies) will capture gains and lead to enhanced long-term returns as long as you don’t trade too often.

Assuming you’ve got all the correct characteristics in place, a ‘good’ portfolio ensures you’ve got adequate exposure to the market while assuming a measured level of risk, tax sensitivity, and an appropriate degree of rebalancing.

At the end of the day, a good portfolio can only succeed if you believe in the strategy and, most importantly, allow it to perform as designed over the long-term. To do this you, you must be certain that it is a good portfolio for you.

Edi Alvarez, CFP®

BS, BEd, MS