The oldest person alive today is Emma Morano of Vercelli, Italy who turned 117 this November. She was born in 1899! Queen Victoria was still on the throne of England and William McKinley was president of the United States. If you’d asked Emma in 1917 if she could imagine living long enough to see 2017, would she have imagined such a long life? Most Americans do not live as long as Emma, but in general we are living longer and healthier lives. The number of centenarians is on the rise. Longevity – long life – can have obvious perks, but also poses a conundrum in terms of finances. To help us plan for longevity we use “longevity risk” to measure the likelihood that you’ll run out of wealth before you’ll run out of life. In our planning we like to ensure that we mindfully set longevity at the right level for each person.

Few, if any of us, have advance knowledge of precisely when our time will come, so questions like this often boil down to statistics. You’ll sometimes hear that the average life expectancy for females is age 83 and age 81 for males, BUT are these appropriate target-end dates for your retirement plan? The truly important challenge is coming up with the best end-dates for retirement that will allow you to enjoy your wealth early while leaving enough assets to comfortably support you later in life.

In retirement planning, the variation in life expectancy can range quite dramatically and yet we find that client expectations generally fall into two categories, (1) those who want to make absolutely sure they don’t outlive their wealth, and (2) those who have a definite expiration date in mind, say 80 years of age, and believe that planning for life beyond that age is simply not relevant or realistic. The latter are often operating on some assumption based on, for example, both parents dying in their late 70s or not long after retirement.

At the risk of sounding morbid, but with the goal of having your retirement plan more fully represent your expected end of life target date, I want you to consider three facts that most often cause people to underestimate their longevity (in turn, this may help you understand why we sometimes encourage you to increase your target-end date):

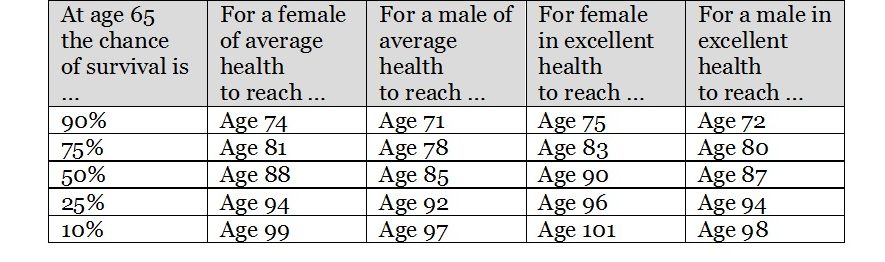

Life expectancies that are often quoted may not be relevant since they are often calculated at birth. Life expectancy on reaching age 60 or 65 should be much higher than those quoted at birth since some will die before they reach this age. In fact, life expectancy for a 65-year-old, non-smoker is much higher. As an example, a 65-year-old female of average health has a 50% chance of reaching age 88 (see the table below) but once she reaches age 88 she has a much higher chance of reaching age 95.

- Life expectancy is often calculated using mortality rates from a fixed year instead of projected to future expected mortality rates. Social Security Administration (SSA)’s period life tables are based on real mortalities in any given year. Though valuable, since they are real, they underestimate the observed trend for increased survival. As mentioned above, we perceive our survival based on our own anecdotal experiences. The question to ask ourselves, is this correct or is this an underestimation?

- Finally, we find that the population on which longevity risk calculations are based may not be appropriate. If we work with an aggregate US population life expectancy (as does the SSA period life tables) we must include a correction for socioeconomic and other factors that are known to impact mortality rates and could underestimate our lifespans. To-date there is evidence to indicate a positive link between income, education, long-term planning, and health. Yes, someone who plans and prepares appears (statistically) to live longer.

In case it is still not clear – let me explain. When planning retirement projections, the length of retirement greatly impacts planning choices (planning for 20 versus 45 years may require different strategies given the same wealth). Considering your specific longevity risk necessitates that we prepare for the contingencies that apply to you. There may be good reasons to target a lower longevity, but for most we will likely need to include, at the very least, a reasonable adjustment for expected increased longevity. This often means distribution of existing assets and thinking about end-of-life questions (a topic most prefer not to address too closely). If you are expecting a longer life, consider accumulating a pool of longevity assets (like some are doing to cover for potential Long-Term Care contingency) or purchasing a longevity annuity (this asset would only be used if you live past a certain age and, therefore, accumulate what are called mortality credits that can provide a good income late in life, but would be lost if you wind up passing sooner).

Obviously, estimations are just that, estimations. Still, a thoughtful scientific approach ought to be the foundation for retirement projections, never speculation or conjecture. Like Emma, some of us will be blessed with a long life, even inadvertently. One way or the other, I want all of us to feel that we’ve had a life well spent, and that will depend largely on how well we’ve planned for possible contingencies in your life.

This educational piece was drawn from my work with clients, www.longevityillustrator.org, the Social Security Administration period life tables, and a recent academic publication by Wade D. Pfau, Ph.D., published in The Journal of Financial Planning, November 2016, vol 29, issue 11, pp 40.

Edi Alvarez, CFP®

BS, BEd, MS